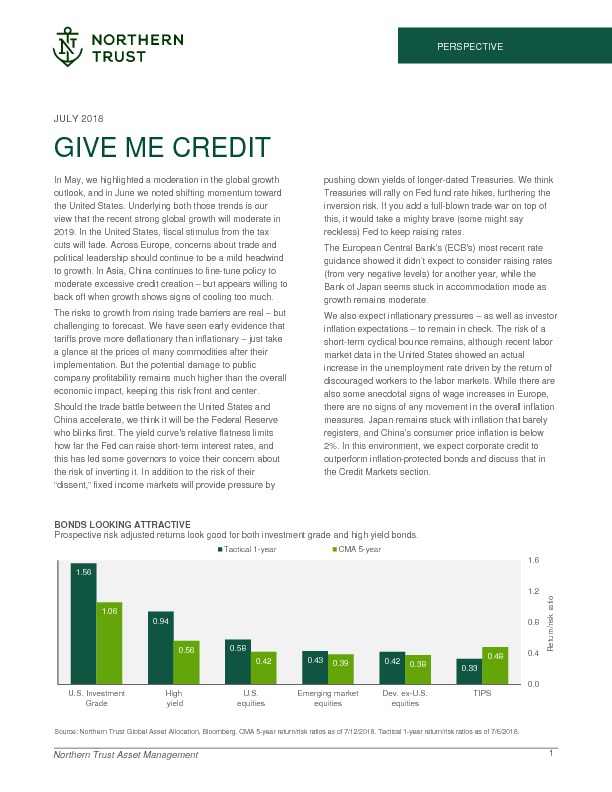

Give me credit

In May, we highlighted a moderation in the global growth outlook, and in June we noted shifting momentum toward the United States. Underlying both those trends is our view that the recent strong global growth will moderate in 2019. In the United States, fiscal stimulus from the tax cuts will fade. Across Europe, concerns about trade and political leadership should continue to be a mild headwind to growth. In Asia, China continues to fine-tune policy to moderate excessive credit creation – but appears willing to back off when growth shows signs of cooling too much.

The risks to growth from rising trade barriers are real – but challenging to forecast. We have seen early evidence that tariffs prove more deflationary than inflationary – just take a glance at the prices of many commodities after their implementation. But the potential damage to public company profitability remains much higher than the overall economic impact, keeping this risk front and center.

Should the trade battle between the United States and China accelerate, we think it will be the Federal Reserve who blinks first. The yield curve’s relative flatness limits how far the Fed can raise short-term interest rates, and this has led some governors to voice their concern about the risk of inverting it.

Om dit artikel te lezen heeft u een abonnement op Investment Officer nodig. Heeft u nog geen abonnement, klik op "Abonneren" voor de verschillende abonnementsregelingen.